This article is an excerpt of the book Open models published in French in 2014 and translated in 2016.

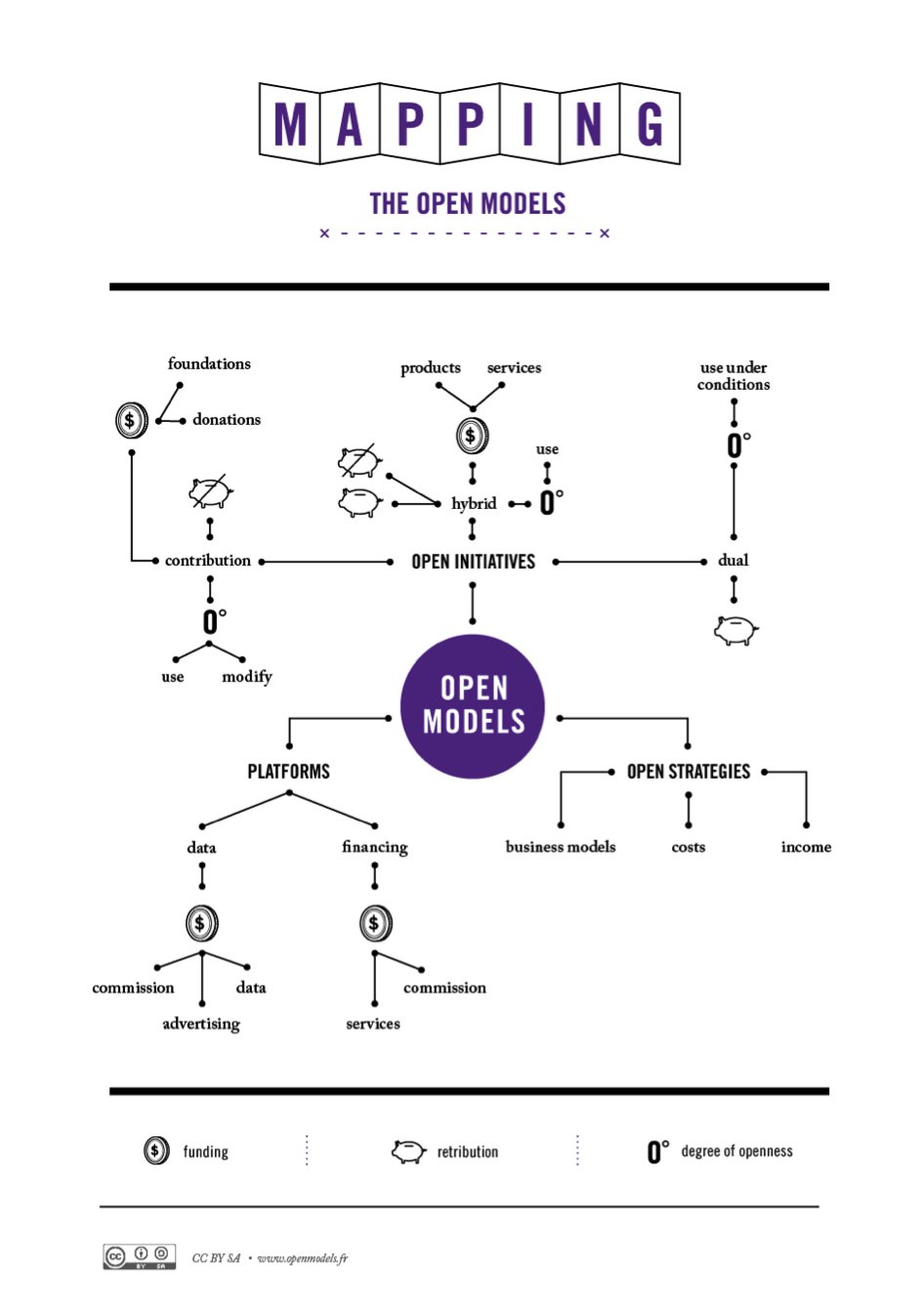

The first conclusion of our work collecting data on open business models is that the “open beyond the open” does indeed exist, to quote Lionel Maurel, one of our contributors. Three areas can be identified: open initiatives, distribution and financing platforms, and players that open part of their model.

In the area of education, this is how these areas could be represented: Khan Academy’s free platform of online courses is an open initiative financed by foundations; Coursera (a platform for the distribution and monetization of university courses online) is part of the open models ecosystem; a Business School that launches a MOOC (Massive Online Open Course) is a traditional player that opens part of its model.

Let’s get into the details…

Open initiatives models

These are initiatives which ever since their inception, chose to be open. They seek to define the feasibility conditions for their project, in particular how to mobilize the resources required to achieve the value proposition offered to recipients. We identified three types of open initiative models: contributory, hybrid and dual.

The contributory model is present in software with Linux, in manufacturing with Protei, and in education with the Khan Academy. In this model, the resources that make up the open asset are provided by non-remunerated volunteer contributors, or by employees who are paid by companies or individual donations. The recipients have free access to the open asset. No monetization occurs from their use of the open asset (no sale of data for advertising purposes, no advertising banners). The contributors who participate in these activities have other income that provides them with the level of resources they need. Companies or universities sometimes play a facilitator role in that they enable some of their salaried employees to allocate time to open initiatives. It is often companies in the sector that finance foundations enabling open initiatives to operate. IBM finances part of the Linux Foundation for example.

In hybrid models, the resources are also provided by volunteer contributors, who are not directly remunerated by the monetization of the open asset. The individuals do however receive an income supplement which is more or less connected to the open asset. This is the case of a lot of software that has been developed and maintained for free by contributors or organizations which then monetize integration or advisory services to companies who use the software. With regard to open manufacturing, it is sometimes the sale of secondary products that generates enough income to finance the teams who work to maintain the open asset. In some examples of open education, it’s the sale of ebooks or textbooks which enables the required financial resources to be generated to remunerate the individuals who develop the open asset.

The third type is dual in the sense that the asset is made available either free of charge, subject to specific conditions or for specific people, or as a paid version under other conditions or for other people. It is an operational approach often found in the Art and Culture space. Some software is free if the users return modification under the same sharing conditions, and is paid if they are not returned. Freemium models are an example of this type and the monetization criteria varies on a case by case basis.

Distribution or financing platforms

The purpose of the previous models is to build an open asset. In order to be financed, when it is not supported by volunteer contributors, and in particular to be distributed, this asset often requires a platform. Distribution or financing platforms can be seen in each of the six areas we have explored.

Whether they are generalist or specialist, crowdfunding platforms provide a solution to the financing issue by connecting projects that need financing with a community ready to fund them. These platforms are remunerated via a commission on the financed amount.

Distribution platforms enable content to be read or shared. In the majority of cases, they are established on a two-sided model, where the audience reached by free consultation of content is monetized by marketers using advertising. Usage data can also be monetized. These two kinds of revenue are found in some open science and open education platforms.

Openness as a strategy

The last area of open business models is that of players whose main aim is not to create or distribute an open asset but who open part of their assets or value chain. This practice is more and more common and is represented in open innovation approaches for example.

In each of the areas we have analyzed, there are openness strategies being implemented by traditional players. These initiatives can be organized into three categories according to their value and the players that implement them.

The main impact of some open initiatives is to grow the income of base or reference model. This is the case when a higher education institution produces a MOOC. The primary motivation is promotion (to make the institution, its staff and programs known). The expected impact is related to the sales of the institution’s base model (student enrolments or company orders for training programs).

Other initiatives enable better use of resources or a reduction in the resources required. They thus have productivity value. These are often the initiatives which mobilize clients in the design phase (crowdsourcing as in aerospace with Boeing or in the car industry with Mu) or in the value chain production stages (carpooling for shopping for example).

Finally, the primary motivation for some initiatives is to trigger or accelerate the transition towards new business models, often in conjunction with the digitization of activities. This is one way of interpreting the investments some institutions make in MOOCs. It is not only about having a communication channel to sell programs, but is also a way of experimenting with other business models, such as the platform model. In this instance, the value of the open initiative is above all an experimental value.

We must also not forget, as has been previously described, that one of the contributions some organizations make is to financially support open initiatives in their sector, not only from a philanthropic perspective but also because it’s good for business (Linux and IBM). Support of open initiatives can sometimes also be used to gain a competitive edge. These indirect openness strategies (indirect, as these groups support open initiatives) sometimes correspond to competitive strategies.

A final openness strategy is that of organizations that use openness to position themselves as players in a bigger chain and to enable other economic players to create value based on the asset that is made available.

The Apple appstore has frequently been described as using this strategy. By making the tools, technical hosting platform and the commercial site for distribution of applications available, Apple has become a platform enabling application developers to build or grow their activity in return for a share of the revenue generated.

These platform strategies (more or less open) are now being implemented in very concrete sectors, and not only in the digital production space.

Tesla and Tabby are two examples from the car industry which illustrate this platform logic.

It’s better to hold 50% of a market of one million vehicles annually than 100% of a market of some tens of thousands of vehicles.

We already mentioned Tesla’s decision to open its intellectual property. In June 2014, Elon Musk announced the following on the company’s site:

“Tesla Motors was created to accelerate the advent of sustainable transport. If we clear a path to the creation of compelling electric vehicles, but then lay intellectual property landmines behind us to inhibit others, we are acting in a manner contrary to that goal. Tesla will not initiate patent lawsuits against anyone who, in good faith, wants to use our technology.”

This decision might seem difficult to understand coming from a listed company, which raised money partly by promising to capture value through its R&D strategy and patent licensing revenue.

Tesla’s decision can in fact be interpreted as a brave strategic movement, yet one that is completely logical from a platform perspective. By opening its technology, Tesla is facilitating access to other players who will help it open up the electric vehicle market. Elon Musk has observed that players in the car industry do not invest enough and have decided not to tip the scales toward an alternative to the dominant combustion engine model. This is evidenced in the very small share of electric vehicles sold (0.41% in April 2014 in France, close to half being the Renault ZOE). As Musk sees it, given that it’s not the current manufacturers that are going to contribute to increasing volumes, the emergence of new players must be supported. With this increase in the number of players and in sales volume, infrastructure costs (recharge stations) will be financed across a broader base. In being open, Tesla fosters the creation and development of competition, but more importantly is creating an opportunity to increase the market’s global volume. To make the point, it’s better to hold 50% of a market of one million vehicles annually than 100% of a market of some tens of thousands of vehicles.

Furthermore, by fostering the emergence of new players that will use its technology and its products, Tesla is positioning itself as the main player (the platform) in the electric vehicle industry and will be in a good position to capture part of the value created by others by becoming a supplier of parts or material, or by becoming a platform for related services.

On a very different level, Tabby also illustrates this platform logic. In the spring of 2014, a car kit without a car body was released on the market by OSVehicle. The vehicle design is open. Anyone can use the plans, manufacture the parts, and make improvements. By putting in place an open model from the outset, OSVehicle is also positioning itself in a platform logic and aims to become the central point of the economy around its vehicle. By enabling other players to build or develop their activity (those that will build car bodies, assemble the car, develop parts or designs for specific use) OSVehicle is facilitating the development of the client market.

In this configuration, OSVehicle’s position will be the platform which will allow all players, depending on their place in the chain, to buy the kits or to offer additional products or services. Exactly as Apple has done with the appstore!

Following the release of this first vehicle, we could envisage that OSVehicle will become a platform for other machines designed by other developers or manufacturers.

Future sectors for open models (or not)

Open models in art and culture, software, industrial design, science and education are shaking up entire sections of our society and this already long list is only a partial one. We can see that other sectors will follow. Some impact us on in an everyday way, others affect us more personally. There are three areas in particular that are moving towards becoming open: money, the living and health.

Cryptocurrencies are multiplying and becoming alternatives to the monetary system that we currently use, where currency is minted by governments. Bitcoin, Riple, Peercoin and others are based on very different foundations. In these peer-to-peer electronic currencies, monetary creation is decentralized to individuals and executed by software which is also decentralized.

In the face of seed privatization by players such as Monsanto, more and more initiatives are starting to offer open seeds, freely available for use, with no fee payments or patent royalties. More broadly, the intellectual property and seed license debate is heated at a national, European and international level.

The health economy is built partly on patents, whether for medication or medical equipment. The debate between economic players, seeking to obtain fees to pay off their investments, on the one hand and players in the health industry chain (patients and financiers), who want to improve access to treatment or lower the cost, on the other, has found a new forum for expression in prostheses. Similar to other growing initiatives which are aimed at mobilizing a community, open models are also emerging in this space, to create open source prostheses.

We can see that open models are growing in number, becoming more widespread and gaining ground. The question is no longer knowing where they will emerge, but at what pace they will develop and under which conditions.

– Translation by Nicola Savage